The Top 4 Tax Issues for Executive Employees

By Matt Held, CFP®

Without capable executive employees, major companies like GE and P&G would not be where they are today. Consequently, many executives receive generous compensation packages that include equity compensation, incentives, bonuses, and top-tier benefits.

These compensation packages often lead to complex tax situations. While it’s generally best to consult a financial advisor for personalized advice, these are four common issues executive employees should be aware of.

1. Equity Compensation

Equity compensation—including restricted stock units (RSUs), performance shares, and incentive stock options (ISOs)—is a major part of the compensation package for most executive employees. However, it can lead to unintended tax consequences like these:

- RSUs are usually taxed as income when they vest.

- Exercising stock options is a taxable event.

- The “bargain element” of ISOs can trigger the alternative minimum tax (AMT).

When RSUs vest or when nonqualified stock options (NSOs) are exercised, companies typically withhold only 22% for federal income tax. For many high-earning executives, this rate is below their actual tax bracket, which means additional tax may be due when filing their return. Being proactive about these potential shortfalls can help prevent surprises at tax time.

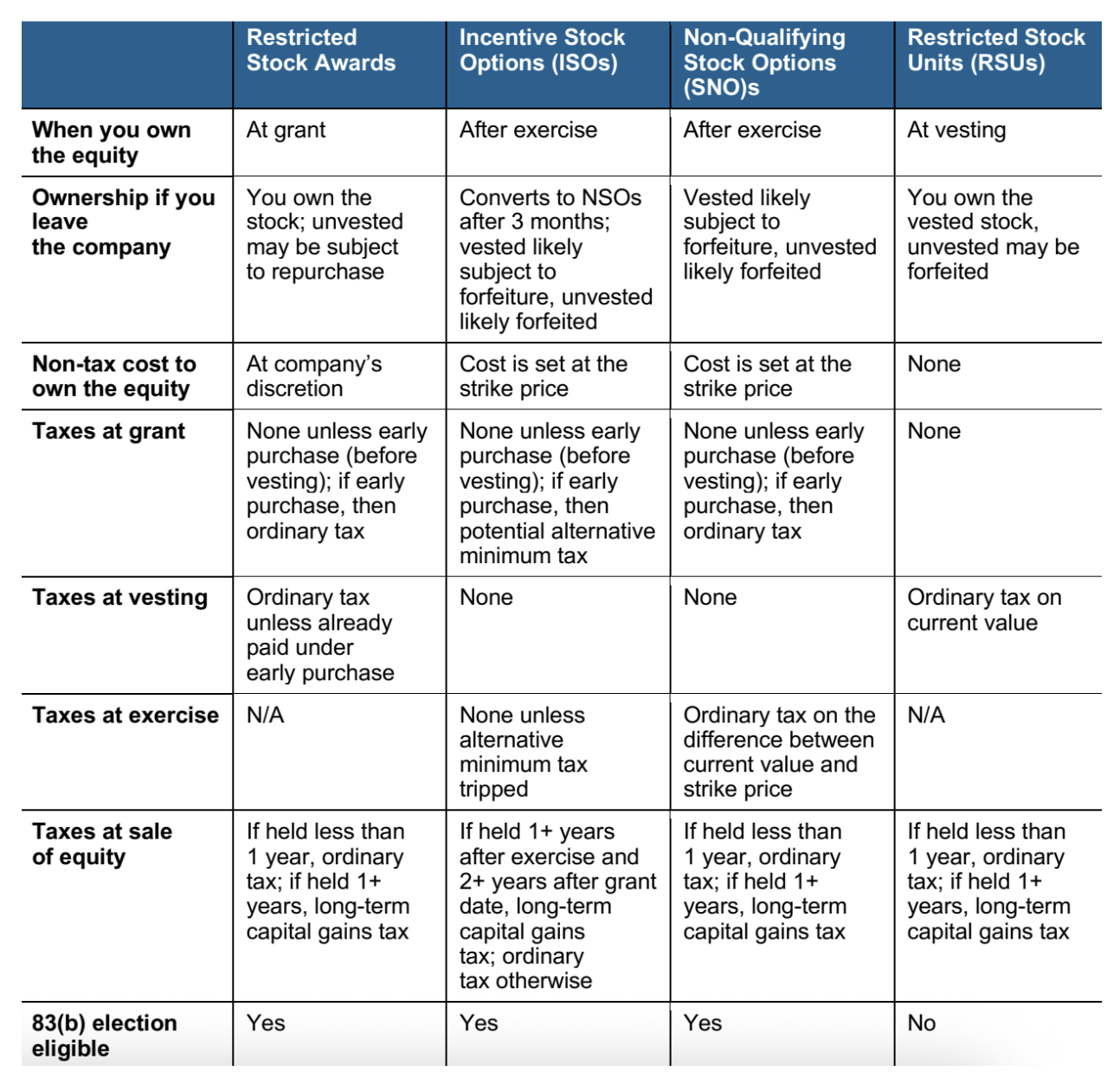

Taxation—Restricted Stock and Stock Options

This chart outlines how various forms of equity compensation are taxed. For personalized guidance, consult your advisor before making any decisions.

With careful financial planning, you may be able to minimize the impact on your tax bill. The earlier you get in touch with us, the greater the likelihood we’ll be able to help.

2. Complex Taxes

Executive employees often deal with tax challenges that many lower-level employees do not. Equity compensation is one example, but it’s far from the only tax concern.

Some executives opt for deferred compensation to avoid being pushed into a higher tax bracket. With this option, an employee receives a portion of their salary after retirement. Compensation is usually taxed when it is received, so they generally pay less in taxes overall. However, this decision can be a gamble. If the employer becomes financially insolvent in the future, the employee may not receive what they’re owed.

3. Multi-Decade Retirement

Many successful executive employees have decades-long retirements. This isn’t necessarily a bad thing. However, lengthy retirements can sometimes come with unforeseen tax consequences.

For example, if an executive employee has a very well-funded 401(k) or other tax-deferred account, required minimum distributions (RMDs) may be significant. RMDs are taxed as income, so some retired executives could pay more in taxes than they had anticipated.

High income taxes aren’t the only concern. If income from RMDs is high enough, Social Security benefits could be taxed. The retiree might also be subject to Income-Related Monthly Adjustment Amount (IRMAA) charges that increase the cost of Medicare Part B and Part D premiums.

4. Major Life Milestones

Major life milestones like marriage, divorce, or the birth of a child can trigger tax complications for anyone. For executive employees, those tax consequences are often extremely complex.

For example, if an executive gets married and both spouses work, they may be pushed into a higher tax bracket. High-earning spouses sometimes don’t withhold enough from their paychecks, so they may end up with an unexpectedly large tax bill.

Post-divorce taxes are often difficult to navigate as well. For example, many divorces involve dividing an executive’s retirement plan between the spouses. If the executive were to withdraw funds and transfer them to their spouse, they would owe significant taxes and penalties.

In most cases, they must obtain a qualified domestic relations order (QDRO) to avoid immediate taxes. A QDRO is a court order requiring the plan administrator to divide the plan between the spouses.

For Executive Employees, Taxes Are Complex

If you’re like many executive employees, you confidently make decisions at work. However, when it comes to taxes, you may be unsure of how to proceed. Clarity Wealth Management is here to help you make sense of this unique tax landscape.

We take a comprehensive, objective approach, and our unique first-year planning fee structure is designed to dovetail with the needs of GE and P&G executive employees.

Interested in a no-obligation, icebreaker call? Schedule online here, call (513) 278-9420, or email Info@ClarityWealth.org.

About Matt

Matt Held, CFP®, is the lead advisor and a founding partner of Clarity Wealth Management, a boutique firm based in Cincinnati, OH. Since entering the industry in 2006, Matt has helped corporate executives, professionals, and business owners uncover opportunities and build long-term financial strategies. Driven by a desire to control his own future and create a lasting brand, Matt co-founded Clarity Wealth Management in 2012. His mission was to build a firm that would provide truly personalized guidance—and become a legacy for his own family. Today, Clarity serves about 100 households and focuses on helping clients simplify and navigate complex financial decisions, particularly those involving equity compensation, tax planning, and executive retirement.

Matt’s approach is rooted in trust, loyalty, and hard work. As a CERTIFIED FINANCIAL PLANNER® professional, he is deeply committed to long-term relationships and believes that clarity doesn’t mean predicting the future, but having the confidence that your plan can handle whatever comes your way.

Outside of work, Matt enjoys time with his wife, Abby, and their twins, Henry and Kinsley. Whether it’s watching sports (they love their Ohio State Buckeyes), hitting the slopes out West, or squeezing in a workout, he’s passionate about staying active and present. He’s also a proud graduate of Moeller High School and The Ohio State University. Matt holds Series 7 and 66 licenses, is licensed for health insurance, and earned his CFP® certification in 2012. He has been named a Five Star Wealth Manager in the Cincinnati area since 2013.* To learn more about Matt, connect with him on LinkedIn.

*2013-2018 and 2020-2024 Five Star Wealth Manager Award, created by Five Star Professional. The 2024 award was presented in September 2024 based on data gathered within 12 months preceding the issue date. Advisors pay a fee to hold out marketing materials. Not indicative of advisor’s future performance. Your experience may vary. For more information, please visit www.fivestarprofessional.com.